Get Legal Advice

(256) 993-5260

Originally published: December 2025 | Reviewed by J. Wesley Atkinson

When you buy a home in Alabama, the closing table can get confusing. You might spot two different title insurance policies and wonder if you really need both—an owner’s policy and a lender’s policy—or if one’s enough.

Here’s the thing: lenders always require their own policy, but buyers need both for full protection of their property investment.

Lender’s title insurance protects only the mortgage company’s financial interest, leaving homeowners exposed to title defects that could threaten their rights.

If you skip the owner’s policy, you could risk losing your home or getting dragged into expensive legal fights over property disputes. Each policy serves a different purpose, so both are crucial for a secure real estate transaction.

Key Takeaways

- Lender’s title insurance protects the mortgage company, while owner’s title insurance protects the buyer’s investment and rights.

- Both are recommended in Alabama because they cover different risks and protect different people in the deal.

- If you skip owner’s title insurance, you could lose property rights or end up paying for expensive legal battles over deeds and claims.

60-Second Answer: Quick Bottom Line

Lender’s title insurance protects the mortgage company’s investment. Owner’s title insurance shields the buyer’s ownership rights.

Most buyers in Alabama end up needing both policies to protect their home purchase from every angle.

Who the Lender’s Policy Covers

The lender’s policy only covers the mortgage company’s financial interest in your property. If title problems pop up, it covers the outstanding loan amount.

What it protects:

- The bank’s mortgage investment

- Loan amount up to the payoff balance

- Lender’s ability to foreclose if necessary

This policy loses value as you pay down your mortgage. Once you pay off your loan, the coverage disappears.

If title issues arise later, the lender is compensated for its loss. Homeowners, though, get nothing from this policy.

The buyer always pays for this coverage, even though it only helps the lender. Mortgage companies almost always require it before they’ll approve your loan.

What the Owner’s Policy Adds

Owner’s title insurance protects your ownership rights and equity in the home. It covers the full purchase price as long as you own the property.

Key protections include:

- Ownership disputes from past owners

- Unpaid liens or judgments against the property

- Boundary line conflicts with neighbors

- Forged deeds or fraudulent transfers

This coverage stays active for as long as you or your heirs own the property. Its value never drops.

Without owner’s coverage, you could face legal fees and even lose your property if a title defect comes up. The risk? Losing your entire investment if something major goes wrong with ownership.

Quick Decision: Do You Need Both?

Lender’s policy: The bank requires it—no way around that.

Owner’s policy: It’s optional, but real estate pros almost always recommend it.

Many buyers choose both policies. The owner’s policy is a one-time premium typically tied to the purchase price and local rate filing—often more than a few hundred dollars on financed purchases..

If you don’t get both:

- Lender gets paid, but you could lose your home

- You pay legal fees out of pocket

- No coverage for ownership disputes

If you get both:

- Everyone’s protected

- Legal defense is included

- Financial compensation for covered losses

Most Alabama buyers decide both policies are worth it. For a small extra cost, you get peace of mind and protection for your biggest investment.

What Is Lender’s Title Insurance & How It Works in Alabama

Lender’s title insurance protects the lender’s financial stake in your property. The coverage amount drops as you pay down the loan, and buyers usually pay for it at closing.

Coverage Period & Limits (Runs Until Loan Is Repaid)

This insurance stays in effect as long as you owe money on your mortgage. The coverage starts at your full loan amount and shrinks as you make payments.

Let’s say you borrow $200,000. The policy covers that to start. If you pay off $50,000, now it covers $150,000.

It makes sense—the lender’s risk drops as you build equity. Less money at stake means less coverage needed.

Once you pay off your mortgage, the lender’s title insurance vanishes because the bank no longer has a claim on your property.

This policy covers title defects that existed before you closed. We’re talking forged documents, undisclosed heirs, or liens that slipped through the cracks during the title search.

Typical Cost Structure in Alabama

In Alabama, who pays is a contract term shaped by local custom. In many counties, sellers often cover the owner’s policy while buyers pay the lender’s—but this is negotiable and can vary by market conditions.

Lender’s title insurance costs depend on your loan amount. Alabama uses a rate schedule, so bigger loans get a slightly better per-dollar rate.

For a $250,000 mortgage, expect to pay around $800 to $1,200 for lender’s title insurance. The price varies by title company and any extra endorsements your lender wants.

Common extra fees:

- Search and exam fees

- Recording fees

- Notary services

- Wire transfer charges

Lenders often want specific endorsements for extra protection—stuff like survey issues or environmental risks.

Why You Can’t Skip the Lender’s Policy When Financed

Mortgage lenders won’t budge on this: lender’s title insurance is required for loan approval. No policy, no loan.

Banks need to know their lien is solid. If title problems show up after closing, they want to be protected.

The policy protects the lender’s right to foreclose if you default. Title defects could block foreclosure or render the property unmarketable, leaving the lender in trouble.

Lenders demand this coverage because they’re putting up big money for properties they’ve never seen or researched themselves. The title insurance company does the heavy lifting on ownership verification.

If you buy with cash and refinance later, you’ll still have to purchase the lender’s title insurance then. The new lender always wants fresh coverage, even if you already have an owner’s policy.

This rule applies in every state and for every loan type—conventional, FHA, VA, jumbo, you name it.

J. Wesley Atkinson, P.C., helps Alabama buyers avoid costly title mistakes and protect their equity before closing. Get clarity on your coverage needs today—contact us.

If you’re ready to get started, call us now!

What Is Owner’s Title Insurance & Why It Matters in Alabama

Owner’s title insurance protects you from financial losses caused by title defects that existed before your purchase but didn’t show up in the title search.

While a lender’s policies only protect the mortgage company, an owner’s policy covers your investment for as long as you own the place.

What It Covers (Hidden Liens, Forgery, Missing Heirs)

This policy covers a range of title defects that could affect your ownership rights. It pays out for problems that happened before you bought the house.

Hidden liens are a big threat—like unpaid contractor bills, tax liens, or judgments against previous owners that slipped through the search.

Forgery and fraud coverage helps if:

- Past deeds have fake signatures

- Someone signed documents without legal authority

- Identity theft affected earlier sales

Undisclosed heirs can show up years later, claiming the house. This happens when a previous owner died without a will or when family members weren’t tracked down during the sale.

The policy also covers survey errors, mistakes in public records, and invalid divorces that could impact your rights.

Owner’s title insurance protects the homeowner’s equity and ownership rights, while a lender’s policy protects only the loan balance—the coverage focus and beneficiaries differ.

How It Differs from Lender’s Policy (Who It Protects, Duration)

The main difference? Who gets protected, and for how long?

Who it protects:

- Owner’s policy protects you and your heirs

- Lender’s policy only protects the mortgage company

Duration:

- Owner’s policy lasts as long as you or your heirs own the property

- Lender’s policy shrinks as you pay the loan and ends when the mortgage is gone

If you refinance, the lender wants a new lender’s policy, but your owner’s policy keeps covering you as long as you own the home.

Coverage amounts differ, too. Owner’s policies usually cover the full purchase price, while lender’s policies only match the loan balance.

Cost & Payment Timing in Alabama

In Alabama real estate deals, the seller usually pays for the owner’s title insurance policy. The buyer covers the lender’s policy.

Payment structure:

- One-time premium paid at closing

- No monthly or annual payments

- Coverage lasts as long as you own the property

The cost usually falls between 0.5% and 1% of the purchase price. So, for a $200,000 home, expect the owner’s policy to run $1,000 to $2,000.

Because sellers traditionally pay for the owner’s policy here, buyers often get this protection without shelling out extra. Still, check your contract—sometimes people negotiate who pays what, and the typical setup might shift.

Timing matters. Title insurance covers only issues that existed before the policy kicks in. If you spot a title problem, file your claim right away.

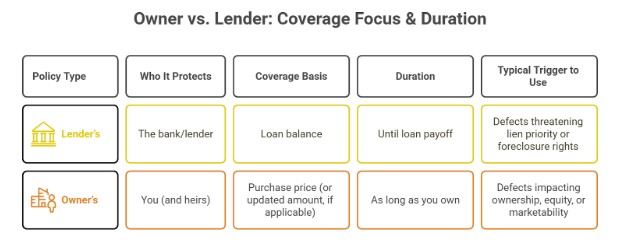

Table A — Owner vs. Lender: Coverage Focus & Duration

| Policy Type | Who It Protects | Coverage Basis | Duration | Typical Trigger to Use |

| Lender’s | The bank/lender | Loan balance | Until the loan payoff | Defects threatening lien priority or foreclosure rights |

| Owner’s | You (and heirs) | Purchase price (or updated amount, if applicable) | As long as you own | Defects impacting ownership, equity, or marketability |

Do You Need Both Policies in Alabama? Decision Guide

Most Alabama homebuyers end up with both owner’s and lender’s title insurance. Cash buyers can be more flexible. County habits and how much equity you have can sway whether you really need both.

Situations Where Both Make Sense

Financed purchases always require a lender’s title insurance. Adding an owner’s policy gives you full protection. If the lender wants coverage, shouldn’t you?

High-value properties in Alabama make both policies worth it. If something goes wrong with a $400,000 title, that’s a nightmare without owner’s insurance.

Properties with messy histories—think lots of owners, estate sales, or foreclosures—really need dual coverage. The risk just goes up.

Investment properties and rentals? Both policies. Landlords run into title headaches that lender’s insurance simply doesn’t touch.

First-time buyers might want both. It’s easy to miss red flags, and paying a little extra can save a lot of pain.

When the Owner’s Policy Might Be Optional (Cash Purchase, Low Equity)

Cash buyers get to choose. No lender, no requirement. You can skip the owner’s title insurance, but it’s a gamble.

Low-equity situations might tempt you to pass on owner’s coverage for now. If you’re stretched thin, you might focus on other costs.

Short-term plans change the math. If you’re selling in a year or two, the premium might not be worth it.

Still, even cash buyers risk a lot without coverage. Alabama’s title insurance offers the same protection no matter how you buy.

Refinancing only triggers a new lender’s policy. Your owner’s coverage stays in place, so you don’t need to double up.

Alabama-Specific Caveats (County Practices, Exemptions)

Recording workflows and document preferences vary by Alabama county. Jefferson and Madison often have streamlined probate-court processes; some rural counties may require additional affidavits or clarifying documents.

Mineral rights can get messy in Alabama. Coal, oil, and gas claims sometimes slip through the cracks—standard policies don’t always catch them.

Homestead exemptions help, but they’re no substitute for real title insurance. They come with their own rules and limits.

Historic homes—especially those built before 1950—often have documentation gaps. That means more title risks.

HOA and covenant problems pop up in newer neighborhoods. Title insurance can shield you from hidden association rules or restrictions.

Table: “Owner vs Lender vs Both – Alabama Decision Matrix”

| Situation | Cash/Financed | Title History | Equity at Risk | Recommended |

| Primary home purchase | Financed | Routine | Medium–High | Both (lender required; owner advised) |

| Investor flip | Financed | Multiple quick transfers | Medium | Both (endorsements matter) |

| Historic/older chain | Any | Gaps/handwritten records | High | Owner’s strongly advised (+ curative steps) |

| Family transfer | Cash | Well-known title | Low–Medium | Consider the Owner’s equity if meaningful |

| Rural acreage/mineral area | Any | Unknown severances | Medium–High | Owner’s + mineral/easement review |

| Situation | Cash/Financed | Title History | Equity at Risk | Recommended |

Cost matters in Alabama real estate. Owner’s policies generally run 0.5-1% of the price, and lender’s policies are a bit cheaper.

Cost, Payments & Who Pays It in Alabama

Standard rates set title insurance prices in Alabama, but who pays depends on the deal. Knowing how this works helps buyers and sellers budget and negotiate.

Typical Alabama Premium Ranges

Title insurance here costs about 0.5% to 1.0% of the sale price for both policies together. On a $200,000 home, that’s $1,000 to $2,000 total.

Premium Examples by Home Value:

- $150,000 home: $750 – $1,500

- $250,000 home: $1,250 – $2,500

- $400,000 home: $2,000 – $4,000

The owner’s policy usually runs a bit higher since it covers the whole purchase price. Lender’s policies only protect the loan.

Recording fees tack on another $15-50 per document. These fees keep the county’s records straight.

Who Typically Pays for Which Policy in Alabama

The seller typically covers the owner’s title insurance in Alabama. It’s a tradition and shows buyers the title’s clean.

Buyers pay for the lender’s policy, which protects the mortgage company. Lenders won’t close without it.

Still, you can negotiate the owner’s policy costs. In hot markets, buyers sometimes offer to pay both just to win the house.

Occasionally, buyers and sellers split the costs. Sometimes buyers pay the full price, especially in bidding wars.

How Cost Impacts Your Closing Outcomes (Equity, Negotiation)

Who pays for title insurance can shape the whole closing. Sellers who pay for the owner’s policy make their homes more appealing by lowering buyer costs.

Buyer Benefits:

- Lower out-of-pocket costs when sellers pay the owner’s policies

- Can put more money toward down payments or upgrades

- More leverage to negotiate other items

Seller Advantages:

- Homes look better to buyers who are watching their budgets

- Faster deals when competition is tight

- Less hassle at closing

It’s smart for both parties to discuss title insurance early. Surprises at closing aren’t fun, and nobody likes last-minute budget headaches.

Choosing between the owner’s and the lender’s coverage shouldn’t be guesswork. Let J. Wesley Atkinson, P.C., review your title commitments and spot hidden risks early—schedule an appointment now.

If you’re ready to get started, call us now!

Risks & Red Flags If You Skip Owner’s Title Insurance

Skipping the owner’s title insurance opens the door to some serious financial trouble. From boundary fights to forged deeds, going without it puts your investment at risk.

Top Title Defects in Alabama Real Estate

Errors in public records haunt plenty of Alabama homes. Decades of handwritten or misfiled paperwork mean mistakes slip in.

Sometimes your deed lists the wrong lot or square footage. Fixing that in court isn’t cheap or quick.

Boundary disputes crop up when old surveys miss the mark. Neighbors might think your land is theirs, especially if fences and maps don’t match.

Rural areas are rife with forged signatures on old deeds. Maybe a relative signed without proper authority, and now you’re tangled in their mess.

Other title headaches:

- Unpaid property taxes from past owners

- Liens from contractors

- Hidden utility easements

- Claims by unknown heirs

Why the Lender’s Policy Won’t Save Your Ownership

Lender’s title insurance protects the bank—not you. It never covers your equity or improvements.

If a title issue arises, the lender’s policy pays off the remaining loan. You still lose your down payment, your renovations, and your house.

For example, if an unknown heir sues, the lender’s policy covers the $200,000 mortgage. You lose your $50,000 down and $30,000 in upgrades.

As you pay off your loan, lender coverage shrinks. Ten years in, it might only cover $150,000 while your home is worth $300,000.

When Title Insurers Refuse Coverage for Missing Owner’s Policy

Underwriters may limit or condition coverage (e.g., by imposing exceptions, higher premiums, or requirements to cure issues) for properties with tangled histories. If one declines, another underwriter may still write, subject to specific exceptions or curative steps.

Red flags for refusal:

- Lots of ownership changes in a short time

- Sales through tax auctions

- Long lists of old liens

- Divorce-related transfers

If one company says no, others usually follow. At that point, selling or refinancing gets nearly impossible until you fix the problems.

If you skip owner’s insurance at closing, you usually can’t buy retroactive coverage for pre-policy defects. Some underwriters may offer a new policy effective from the date of issuance rather than the original purchase date.

Over time, these properties become harder to sell and their value declines.

How to Choose the Right Policy (Checklist for Alabama Buyers)

Buyers really need to weigh their finances and risk comfort when picking title insurance. Asking the right questions and digging into the documents can help you decide whether the owner’s policy is worth it beyond what the lender requires.

Pre-Closing Questions to Ask Your Attorney

Buyers should set up a real conversation with their real estate attorney before closing day. The attorney can walk you through how title insurance policies protect different interests in the transaction.

Key Questions to Ask:

- What specific risks does an owner’s title insurance cover that the lender’s policy doesn’t?

- How much will the owner’s policy cost compared to the property value?

- Are there any known title issues from the preliminary search?

- What endorsements might be needed for this specific property?

The attorney should explain how the title insurance company handles claims and what documentation they’ll want. They can also clarify which party pays for each policy type in Alabama.

Buyers need to understand the difference between one-time premiums and ongoing coverage. The attorney can share examples of real title problems that have hit similar properties nearby.

Reviewing Your Title-Commitment Form

The title commitment document shows what the title insurance company found during its research. Buyers really should read this form carefully before deciding on coverage levels.

Important Sections to Review:

| Section | What to Look For |

| Schedule A | Property description and ownership details |

| Schedule B-I | Requirements that must be met before closing |

| Schedule B-II | Exceptions not covered by the policy |

The commitment lists results from title searches going back decades. Any liens, easements, or ownership disputes show up here.

Buyers should pay close attention to Schedule B-II exceptions. These items won’t be covered, even with the owner’s title insurance.

Common exceptions include boundary disputes, unrecorded easements, and specific types of liens. The form also lists the policy amount and premium costs.

Buyers can use this info to weigh the financial protection against the upfront cost. It’s not always a simple decision, is it?

Attorney’s Recommendations (Why J. Wesley Atkinson, P.C. Recommends Owner’s Policy)

J. Wesley Atkinson strongly advocates for owner’s title insurance because it gives homeowners crucial protection that lender’s policies simply can’t.

His firm has seen firsthand how both policies create stronger legal positions and broader coverage for property buyers in North Alabama.

Legal Leverage When You Have Both Policies

Having both the owner’s and the lender’s title insurance policies gives property owners a real defense system. When title disputes arise, the owner’s policy provides independent legal representation that works for the homeowner—no one else.

The lender’s policy only protects the mortgage company’s financial stake. It doesn’t cover the homeowner’s equity or investment in the property, leaving a significant protection gap that can cost thousands.

Key advantages of dual coverage:

- Two separate legal teams are working on title issues

- Full property value protection instead of just the loan amount

- Independent claims processes that don’t conflict

- Broader coverage for different types of title defects

Alabama law allows for both policies, and most title companies can issue them at the same time during closing. The cost difference is usually small compared to what you could lose.

What We Do in Our Review Process

Atkinson Law conducts thorough title examinations to identify potential issues before closing. The firm reviews property records, surveys, and legal documents to catch problems early.

During the review, they look for common Alabama title issues, such as improper deed transfers, outstanding liens, and boundary disputes. They also check for estate-related problems that could affect ownership rights.

Their review process includes:

- Chain of title analysis – Verifying ownership history back 30+ years

- Lien searches – Finding unpaid taxes, contractor bills, or judgments

- Survey review – Checking property boundaries and easements

- Estate documentation – Making sure inheritance transfers are handled right

When issues come up, the firm works with clients to resolve them before closing. This hands-on approach prevents plenty of title problems that insurance would otherwise need to cover.

When You May Waive Owner’s Policy (With Full Risk Acceptance)

Some buyers decide to skip owner’s title insurance, even though the risks are real. Atkinson Law lays out these risks so clients can weigh their options.

Cash buyers often don’t bother with owner’s policies because no lender is pushing for them. Still, the title risks don’t magically disappear just because you’re paying cash.

Situations where buyers might waive coverage:

- Transfers between family members who know the property’s history

- Properties held for years with a squeaky-clean title record

- Buyers on tight budgets who are okay with the gamble

- Investors who figure the risk is worth it

Risks of waiving the owner’s policy:

- You take on full personal liability for any title defects

- No legal help if a dispute pops up

- You could lose your entire property investment

- All costs for title issues come out of your own pocket

Your home deserves full protection, not partial coverage. Secure your ownership rights and avoid future disputes with guidance from J. Wesley Atkinson, P.C. Start your review today—contact us.

Contact Us Today For An Appointment

Frequently Asked Questions

Do I need both the owner’s and the lender’s title insurance in Alabama?

If you finance, the lender’s policy is required. An owner’s policy is optional but protects your ownership and equity. Together, they cover different risks.

What’s the difference between the two policies?

The lender’s policy protects the bank’s loan balance; the owner’s policy protects your ownership, equity, and resale: different beneficiaries, different triggers, complementary coverage.

How long does each policy last?

The lender’s policy remains in effect until the mortgage is paid off. The owner’s policy is a one-time premium that protects you (and typically heirs) as long as you own.

Who pays for title insurance in Alabama?

It’s contract-dependent. In many counties, sellers often cover the owner’s policy and buyers cover the lender’s, but customs vary and terms are negotiable.

Can I add an owner’s policy later if I skipped it at closing?

Sometimes—but coverage generally applies from the new issuance date forward, not retroactively to your purchase. Check with the underwriter and your attorney.

How much do these policies cost?

They’re one-time premiums based on Alabama rate filings: owner’s tied to purchase price, lender’s to loan amount. Endorsements, search/exam, and recording fees are extra.

What risks does an owner’s policy typically cover in Alabama?

Hidden liens, unknown heirs, errors in public records, forgery/fraud, and many survey/boundary issues. Mineral rights or easement exceptions may require specific endorsements.