Get Legal Advice

(256) 993-5260

Originally published: March 2026 | Reviewed by J. Wesley Atkinson

Owner-backed financing in Alabama — also called seller financing — transfers property without institutional lender oversight, creating serious legal exposure when closing documents are drafted incorrectly, executed out of sequence, or recorded late.

Alabama Code §§ 40-22-1 through 40-22-12 govern the recording of conditional sale contracts in Alabama, and a seller who fails to record the purchase money mortgage at the same closing session as the deed loses lien priority to any creditor who records first.

Identifying the correct document sequence, the due-on-sale clause risk in wraparound deals, and Alabama’s buyer and seller default remedies before closing eliminates the legal exposure that generic online templates routinely create.

Structuring a seller-financed deal in North Alabama? Atkinson Law reviews every closing document before signing to protect your lien position and title rights. Schedule a consultation today.

Owner-Backed Financing in Alabama: Two Legal Structures, One Set of Unforgiving Rules

Owner-backed financing is a real estate transaction structure in which the property seller acts as the lender, the buyer executes a promissory note for the unpaid purchase price, and the seller’s security interest is created either through a recorded purchase money mortgage or a retained-title land installment contract governed by Alabama Code § 40-22-1.

Alabama seller-financed closings use one of two legal structures. Each structure creates different rights, different recording obligations, and different default remedies.

The seller takes back mortgage transfers legal title to the buyer at closing. The buyer simultaneously executes a promissory note for the unpaid purchase price and a purchase money mortgage back to the seller.

The seller holds a recorded lien on the transferred property but no longer holds title. The buyer can sell or refinance the property — but must satisfy the seller’s lien at that event.

The contract for deed — also called a land installment contract or installment sale contract — retains legal title in the seller until the buyer completes all payments. The buyer holds only an equitable interest during the repayment period.

The buyer cannot sell, refinance, or encumber the property until the seller delivers a deed at full payoff.

Both structures share one critical vulnerability: no institutional lender reviews the document package for compliance errors.

Every closing document must be correctly drafted, executed in the right legal sequence, and delivered to the county probate judge’s recording office on time.

Alabama buyers and sellers who rely on generic online templates regularly discover drafting or sequencing errors only after a default occurs, when correcting those errors requires litigation rather than a single filing.

A North Alabama real estate closing attorney reviews the full document package before a single page is signed, identifying sequencing and drafting defects before they become costly title disputes.

The Seller-Finance Document Stack: Six Instruments, Six Points of Failure

A seller-financed closing in Alabama requires six documents: a deed, a promissory note, a purchase money mortgage or conditional sale contract, a closing disclosure, and a title insurance commitment.

Omitting or mis-executing any one instrument can render the seller’s security interest unenforceable, strip the buyer of title protection, or leave both parties without a binding record of the agreed financial terms.

| Document | Legal Function | Recorded at Probate? | Executing Party | Consequence of Omission or Error |

| Warranty or Quitclaim Deed | Transfers legal title from seller to buyer | Yes — county probate court | Seller | Title does not transfer; buyer acquires no ownership interest |

| Promissory Note | Creates a buyer’s enforceable repayment obligation | No — private instrument | Buyer | No legally enforceable debt exists between buyer and seller |

| Purchase Money Mortgage | Secures the promissory note; grants the seller nonjudicial foreclosure rights | Yes — county probate court | Buyer | Seller’s lien is unenforceable against subsequent creditors and third-party purchasers |

| Conditional Sale Contract | Governs installment payments; seller retains legal title until payoff | Yes — within 30 days (Ala. Code § 40-22-1) | Buyer and Seller | Buyer’s equitable interest is unrecorded and vulnerable to third-party claims |

| Closing Disclosure / Settlement Statement | Provides a binding financial accounting of all transaction terms | No — retained by parties | Buyer and Seller | No authoritative record of agreed payment terms, credits, or allocations |

| Title Insurance Commitment | Documents the basis for issuing an insurable title policy | No — policy issued post-closing | Title agent | Buyer and seller bear undisclosed title defect risk with no policy coverage |

Choosing between a warranty deed and a quitclaim deed represents one of the most consequential drafting decisions in a seller-financed transaction.

A general warranty deed obligates the seller to defend the buyer’s title against all past and future claims.

A quitclaim deed transfers only the seller’s existing interest, without any title warranty. The legal distinction between quitclaim and warranty deeds in Alabama determines the scope of the seller’s post-closing title liability and must be resolved before the document package is drafted.

If you’re ready to get started, call us now!

Recording Order at the Alabama Probate Office: Why Sequence Controls Lien Priority

Alabama follows a race-notice recording framework under which the first party to record a real property instrument without notice of prior unrecorded interests acquires priority over all competing claims.

In a seller-financed Alabama closing, the warranty deed and the purchase money mortgage must be recorded at the county probate office in immediate sequence during the same closing session — so no creditor, judgment lien, or subsequent purchaser can insert a competing instrument in the gap between the two recordings.

The correct four-step recording sequence for every seller-financed Alabama closing:

- Confirm the seller’s existing mortgage payoff. Transmit the payoff amount to the original lender and obtain written confirmation that the recorded mortgage release or satisfaction will be filed before — or simultaneously with — the new deed.

- Record the Warranty Deed from seller to buyer at the county probate court. The deed establishes the buyer’s legal ownership and opens the chain of title for the new purchase money mortgage.

- Record the Purchase Money Mortgage from buyer to seller at the same closing session, immediately following the deed. Submit both instruments together so no gap exists in the recording queue that a competing creditor could exploit.

- Record the Conditional Sale Contract at the county probate judge’s office if the transaction uses a land contract structure.Alabama Code § 40-22-1 governs this recording requirement. Alabama attorneys recommend recording within 30 days of execution to protect the buyer’s equitable interest against third-party claims.

Three Recording Failures That Destroy Lien Priority

- The deed records at the probate office, but the seller’s purchase money mortgage does not record at the same closing session. Any judgment creditor, mechanic’s lien holder, or subsequent purchaser who records in that gap acquires priority over the seller’s security interest — leaving the seller holding an unsecured promissory note with no enforceable collateral.

- The conditional sale contract records late or not at all. The buyer’s equitable interest remains invisible on the public record. A subsequent purchaser who acquires the property from the seller without actual notice of the installment agreement takes the property free of the buyer’s interest.

- The seller’s existing mortgage has not paid off before the deed records. The original lender’s due-on-sale clause activates immediately upon recording of the deed, and the lender may demand full repayment of the outstanding loan balance — a payoff demand that can collapse the transaction and expose both buyer and seller to simultaneous financial loss.

When an Alabama attorney discovers a recording sequence error after closing, the standard corrective instrument is a corrective deed filed at the Alabama probate office.

A corrective deed does not retroactively eliminate lien priority disputes that arose during the gap between the original defective recording and the corrective filing.

Recording errors in seller-financed Alabama closings permanently eliminate lien priority. Atkinson Law sequences and records every North Alabama seller-finance closing correctly. Contact us before you sign.

If you’re ready to get started, call us now!

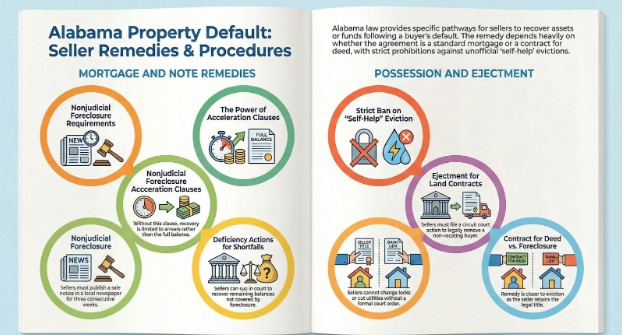

Default Remedies in Alabama: Statutory Rights for Buyers and Sellers When a Seller-Financed Deal Fails

Alabama law provides sellers in a take-back mortgage default with nonjudicial foreclosure rights under Alabama Code §§ 35-10-1 through 35-10-30, requiring three consecutive weeks of published notice before a foreclosure sale.

Alabama sellers in a land contract default may pursue forfeiture and eviction without full foreclosure proceedings.

Alabama buyers facing seller default have specific performance rights enforceable in equity and may file a lis pendens with the county probate office to immediately cloud the title.

Alabama law provides sellers in a take-back mortgage default with nonjudicial foreclosure rights under Alabama Code §§ 35-10-1 through 35-10-30, requiring three consecutive weeks of published notice before a foreclosure sale.

Alabama sellers in a land contract default may pursue forfeiture and eviction without full foreclosure proceedings.

Alabama buyers facing seller default have specific performance rights enforceable in equity and may file a lis pendens with the county probate office to immediately cloud title.

Remedies Available To The Seller When The Buyer Defaults

- Nonjudicial foreclosure (take-back mortgage). Alabama law allows a seller to foreclose without filing a court action. The seller typically must publish notice of the foreclosure sale in a newspaper of general circulation in the county where the property is located for three consecutive weeks before the sale date.

- Direct notice to the buyer (often contractual). Alabama law generally does not impose a statutory requirement to mail direct notice to the defaulting buyer, but many well-drafted promissory notes require a written breach letter before acceleration.

- Acceleration clause. An acceleration clause in the promissory note allows the seller to declare the entire remaining balance immediately due upon default, rather than collecting only the missed installments.

- No acceleration clause limits recovery. If the promissory note omits an acceleration clause, the seller’s recovery at a foreclosure sale can be limited to the arrears amount, not the full payoff balance.

- Deficiency action. If foreclosure sale proceeds do not satisfy the note balance, the seller may sue for the deficiency through a separate Alabama court action. Delays can jeopardize or extinguish the right to recover the shortfall.

- Contract for deed. Under a contract for deed, the seller retains legal title, so the remedy is often closer to eviction than foreclosure.

- No self-help eviction. Alabama prohibits self-help eviction. The seller cannot change locks, remove belongings, or cut utilities without a court order.

- Ejectment for possession. If the buyer refuses to vacate after the land contract is formally terminated, the seller must file an Alabama ejectment action in the appropriate circuit court to obtain an order of possession.

Remedies Available To The Buyer When The Seller Defaults

- What counts as seller default (seller-financed transaction). A seller may default by:

- refusing to execute and deliver a deed after the buyer completes payments

- transferring the property to a third party while the installment contract remains in force

- failing to deliver a marketable title at the agreed closing date

- Specific performance. The buyer’s primary remedy is often specific performance when the seller refuses to close or refuses to deliver a deed at payoff. Alabama circuit courts commonly grant this relief based on the principle that money damages cannot replace a unique parcel of real property.

- Lis pendens. A lis pendens is a notice of pending litigation that the buyer records at the county probate office before or when filing a specific performance action.

- Effect of lis pendens. Recording a lis pendens clouds the title and flags litigation to title searches, buyers, and lenders, typically preventing the seller from reselling or refinancing during the case.

If you’re ready to get started, call us now!

What Alabama Law Requires in 7 Common Seller-Finance Scenarios

Each scenario below identifies a specific trigger event, its legal consequence under Alabama law, and the governing statute or legal authority — so buyers, sellers, and their attorneys can identify the applicable rule before the situation arises.

| Trigger Scenario | Legal Consequence | Alabama Authority |

| Seller records the warranty deed, but delays recording the purchase money mortgage | Any judgment creditor, mechanic’s lien holder, or subsequent purchaser who records in that gap acquires lien priority over the seller’s security interest under Alabama’s race-notice recording framework | Alabama race-notice recording law; Ala. Code § 40-21-1 et seq. |

| Buyer defaults on a land installment contract and refuses to vacate after formal termination | Seller must file an ejectment action in the circuit court — self-help eviction, including lock changes and utility shutoffs, is not permitted under Alabama law | Alabama Title 6, Chapter 6 (Ejectment) |

| Seller dies before the promissory note reaches full payoff | Buyer must obtain the deed through the seller’s Alabama probate estate; if heirs dispute the transfer, buyer may require a quiet title action under Alabama Code § 6-6-540 | Ala. Code § 6-6-540; Alabama Probate Code |

| Seller’s existing mortgage includes a due-on-sale clause, and the seller transfers the property without the lender’s consent | The original lender may accelerate the full outstanding loan balance immediately upon recording of the new deed, regardless of whether the buyer knew about the clause | Garn-St. Germain Depository Institutions Act of 1982; Alabama courts’ consistent enforcement |

| Buyer fails to pay Alabama property taxes after taking possession under a seller-financed land contract | State and federal tax liens attach to the property and may achieve priority over a seller’s purchase money mortgage that was not recorded promptly at closing | IRS lien priority rules; Alabama Department of Revenue lien statutes |

| Seller structures residential owner financing without Mortgage Loan Originator (MLO) compliance | Seller faces federal penalties imposed by the Consumer Financial Protection Bureau (CFPB), and the promissory note terms may be unenforceable against a defaulting buyer | Dodd-Frank Act of 2010, 12 U.S.C. § 5301; CFPB Regulation Z, 12 C.F.R. § 1026.36 |

| Foreclosure sale proceeds are insufficient to cover the outstanding promissory note balance | Seller may pursue the buyer for the deficiency amount through a separate Alabama court action, but must file within the applicable limitations period after the foreclosure sale date | Alabama deficiency judgment statutes; Ala. Code §§ 35-10-1 through 35-10-30 |

Six Hidden Risks In Alabama Seller-Financed Transactions National Guides Often Miss

- Seller estate risk: If the seller dies before payoff, the buyer may have to deal with Alabama probate and uncooperative heirs to get a clean deed.

- Tax lien priority risk: Unpaid property taxes can result in state or IRS liens that may take precedence over an unrecorded or late-recorded purchase-money mortgage.

- Title insurance gaps: Some underwriters add extra requirements for seller financing. Buyers sometimes learn at payoff that no real owner’s policy was issued.

- Balloon payment default: Notes often amortize long-term but balloon in 3–7 years. If the buyer cannot refinance, the seller must choose a workout versus foreclosure.

- Dodd-Frank and Reg Z compliance: Seller financing on a primary residence can trigger MLO and federal compliance requirements. Noncompliance can result in penalties and enforcement actions.

- No institutional oversight: Without a bank-style compliance review, drafting and recording errors can sit unnoticed until default, then require litigation to fix.

Pre-Closing Verification: What Alabama Sellers and Buyers Must Confirm Before Signing

Alabama sellers in a seller-financed transaction must resolve all existing liens, obtain attorney-drafted documents, and record the purchase money mortgage at the same closing session as the deed.

Alabama buyers must confirm a clean title, verify that the conditional sale contract will be recorded within the Alabama Code § 40-22-1 window, and document a refinance strategy before signing any promissory note with a balloon-payment provision.

Seller Pre-Closing Checklist

- Identify and resolve all existing liens. Contact the original lender to obtain a payoff statement and confirm whether the existing mortgage includes a due-on-sale clause that prohibits seller-financed transfers.

- Retain a licensed Alabama real estate attorney to draft the promissory note and purchase money mortgage. Generic online templates omit the Alabama-specific language — including acceleration clauses, cure periods, and foreclosure notice provisions — that Alabama courts require in default and foreclosure proceedings.

- Conduct an independent buyer creditworthiness review. Obtain the buyer’s credit report, two years of income documentation, and verification of the down payment. The seller assumes every underwriting risk that an institutional lender would otherwise absorb.

- Require the buyer to maintain homeowner’s hazard insurance on the property throughout the loan term, with the seller named as loss payee and additional insured on the policy.

- Include four protective provisions in every seller-financed promissory note: an acceleration clause, a cure period of no fewer than 30 days, a late payment penalty, and a due-on-resale provision.

- Submit the warranty deed and purchase money mortgage to the county probate office at the same closing session. Do not permit any recording gap between the two instruments.

- Obtain a title search confirming the take-back mortgage will record in the first lien position. Any unrecorded prior lien that has not surfaced in that search will take priority over the seller’s mortgage at default.

Buyer Pre-Closing Checklist

- Verify that the seller holds a clear title, or confirm that all existing liens will be paid off and released at closing. Review Alabama closing costs in Huntsville and Decatur to accurately budget recording fees, title search costs, and lien payoff amounts.

- Obtain a full title search from a licensed Alabama title agent and request an owner’s title insurance policy. Ask the title agent in writing whether standard owner’s coverage applies to the specific seller-financed structure proposed.

- Confirm that the conditional sale contract or purchase money mortgage will be recorded at the county probate office within the timeframe required by Alabama Code § 40-22-1. Do not take physical possession of the property under a land contract before confirming the contract is on the public record at the probate office.

- Document a balloon payment refinance strategy before executing the promissory note. Identify a lender, verify the property’s projected value at the balloon date, and confirm the buyer’s credit profile supports institutional refinancing.

- Confirm Dodd-Frank Act MLO compliance if financing a primary residence. A promissory note that violates federal MLO requirements may be legally unenforceable.

- If considering a mail-away or remote closing format, review the document-handling requirements specific to Alabama remote real estate closings before agreeing to that format. Remote closings introduce risks to notarization sequencing and delivery timing that require attorney coordination.

Seller financing closes fast — and document defects surface slowly. Atkinson Law, P.C. structures and closes seller-financed transactions for buyers and sellers throughout North Alabama. Schedule your consultation now.

Contact Us Today For An Appointment

Frequently Asked Questions

Does a seller-financed mortgage need to be recorded in Alabama?

Yes. A seller-financed purchase-money mortgage should be recorded in the county probate office to protect priority against third parties. If it is not recorded, a later creditor or purchaser who records first, without notice, can gain superior lien priority under Alabama’s race-notice system.

What happens if a buyer defaults on a seller-financed contract for deed in Alabama?

In a contract for deed, the seller may terminate the buyer’s equitable interest if statutory notice requirements are followed, then seek possession. If the buyer will not leave after termination, the seller typically must file an ejectment action in the Alabama circuit court.

Can a seller in Alabama wrap an existing mortgage in a seller-finance transaction?

Yes, but it is risky. A wrap can trigger the lender’s due-on-sale clause in most conventional mortgages, including conforming loans, allowing the lender to call the loan due. FHA and VA loans may be assumable with lender approval, so the existing loan terms must be verified before the contract is executed.

What is the recording deadline for a conditional sale contract in Alabama?

Alabama law requires conditional sale contracts to be recorded in the county probate judge’s office. Many Alabama real estate attorneys recommend recording within about 30 days of signing to ensure the buyer’s interest appears in the public record and is protected against later claims.

Is owner financing legal in Alabama when the property is the buyer’s primary residence?

Yes, but federal rules can apply. Dodd-Frank and related CFPB rules may require Mortgage Loan Originator compliance for certain seller-financed primary-residence transactions. Noncompliance can expose the buyer to federal penalties and complicate enforcement if the buyer defaults.

What remedy does an Alabama buyer have if the seller refuses to deliver a deed after full payoff?

The buyer can sue for specific performance in the Alabama circuit court to compel delivery of the deed because real property is considered unique. The buyer can also record a lis pendens in the county probate office to cloud title and block resale or refinancing during the lawsuit.

Disclaimer: This article is for general informational purposes only and does not constitute legal advice. Alabama property owners, buyers, and sellers considering a seller-financed transaction should consult J. Wesley Atkinson or another licensed Alabama real estate attorney before executing any closing documents.