Get Legal Advice

(256) 993-5260

Originally published: December 2025 | Reviewed by J. Wesley Atkinson

In Huntsville (Madison County) and Decatur (Morgan County), buyers typically pay 2%–5% in closing costs while sellers usually pay 6%–10%, mostly due to agent commissions.

Local fees vary by county recording costs, title company rates, and loan type — the tables below break down every cost line by line for both cities.

If you know these costs ahead of time, you can budget smarter and avoid that last-minute sticker shock at the closing table.

Fees aren’t the same in Madison County as they are in Morgan County. You might reduce what you owe by using local programs or seller concessions.

Knowing the breakdown for buyers and sellers in each area? That gives you a leg up when you’re making offers or listing your place.

Key Takeaways

- Closing costs in Huntsville and Decatur usually run 2% to 5% for buyers, 6% to 10% for sellers (including commissions).

- Fees shift between Madison County and Morgan County—think different recording fees and transfer taxes.

- Both buyers and sellers can cut closing costs with lender credits, seller concessions, or local assistance programs.

How Much Are Closing Costs In Huntsville & Decatur In 2025?

Buyers in Huntsville and Decatur typically pay closing costs ranging from 2% to 5% of the home price. Sellers pay more—typically 6% to 10%—once you tally up all the fees.

So, for a $300,000 home, buyers might pay $6,000 to $15,000 in closing costs. Sellers? They’re looking at $18,000 to $30,000, with most of that going straight to real estate agent commissions.

Alabama closing costs average 1.38% of the home’s price, which is actually below the national average.

Key factors that affect closing fees include:

- Loan amount and type

- Property value

- Lender requirements

- Title insurance rates

- Local transfer taxes

Buyers in Huntsville and Decatur encounter similar closing costs. The big three for buyers are the loan origination fee, escrow account setup, and appraisal fee.

In Alabama, real estate attorneys or title companies handle closings. You’ll want to budget for attorney fees or title company charges as part of the total.

The actual amount depends on the property, your lender, and whatever you and the other party negotiate. You can knock these costs down with lender credits or seller concessions.

| Party | Typical % of Home Price | Estimated Cost on $300K | What’s Included |

| Buyer | 2% – 5% | $6,000 – $15,000 | Loan origination, appraisal, lender title policy, prepaids (taxes/insurance) |

| Seller | 6% – 10% | $18,000 – $30,000 | Agent commissions, owner’s title, prorated taxes, transfer/recording fees |

Unexpected closing costs can drain your savings fast. Gain confidence, reduce worry, and make decisions without guessing. Get reliable support every step of the way with J. Wesley Atkinson. Contact us.

If you’re ready to get started, call us now!

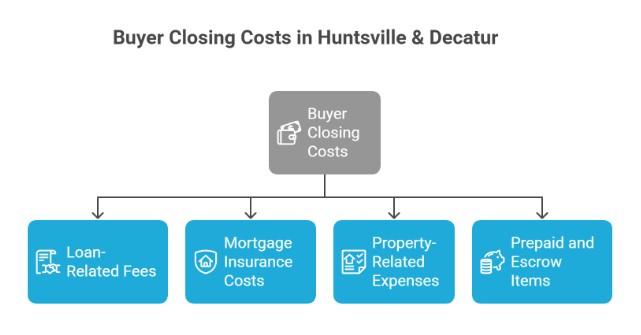

What Do Buyers Pay At Closing In Huntsville & Decatur?

Buyers in Huntsville and Decatur usually pay 2% to 5% of the purchase price in closing costs. These fees cover everything from the mortgage process to the property transfer.

Loan-Related Fees

Buyers pick up the tab for loan origination and processing. The origination fee covers the lender’s processing of your loan application.

You’ll also see an underwriting fee—that’s the lender checking your finances and approving the loan. There’s an appraisal fee to determine the property’s value and a credit report fee for pulling your credit. Don’t forget the processing fee for paperwork.

Discount points let you pay up front to score a lower interest rate. Not everyone does this, but it can make your monthly payments easier to manage.

Mortgage Insurance Costs

Your loan type decides what mortgage insurance you’ll pay. FHA loans require an upfront mortgage insurance premium (UFMIP) and a monthly MIP.

If you’re putting down less than 20% on a conventional loan, you’ll pay PMI. VA loans skip mortgage insurance but charge a funding fee. USDA loans come with their own upfront and monthly guarantee fees.

Property-Related Expenses

Buyers pay for title insurance to protect against ownership disputes. Title search fees cover checking public records for liens or claims.

Attorney fees sometimes come into play if you need legal representation. And don’t forget the home inspection fee—worth it for peace of mind.

Prepaid and Escrow Items

You’ll need to fund an escrow account for future property taxes and homeowners’ insurance. The insurance premium for the first year gets paid up front.

Prepaid interest covers the gap between closing and your first mortgage payment. If you’re buying into an HOA, you might pay some HOA fees at closing, usually prorated to your move-in date.

What Do Sellers Pay At Closing In Huntsville & Decatur?

Sellers in Huntsville and Decatur typically shell out 6% to 10% of the home’s sale price for closing costs. The biggest hit is the real estate agent commission—usually 5% to 6% of the sale price.

Main Seller Closing Costs:

- Real Estate Commissions: 5-6% of sale price (covers both buyer’s and seller’s agents)

- Transfer Tax/Deed Stamps: Varies by county, usually $0.50 per $500 of sale price in Alabama

- Title Insurance: Owner’s policy for the buyer

- Recording Fee: $25-$100 to record the deed transfer

- Property Taxes: Prorated for the time you owned the home during the year

- Closing Agent Fees: Attorney or title company fees for handling the transaction

In Alabama, sellers usually pay for the owner’s title insurance policy. The closing agent ensures the transaction runs smoothly and that all paperwork is in order.

If you agree to pay some of the buyer’s closing costs—seller concessions—your total could go up by 1% to 3% of the price.

Typical seller closing costs in Alabama include title and closing service fees and the transfer tax. The exact numbers depend on your home’s price and what you and the buyer agree to.

Every deal is a little different. Sellers should always ask their closing agent for a detailed closing statement before the big day.

Buyer Vs. Seller: Who Pays What In Madison Vs. Morgan County?

In Madison County (Huntsville) and Morgan County (Decatur), buyers and sellers split closing costs, and the breakdown is similar because both counties are in Alabama.

Typical Buyer Costs:

- Loan origination fees

- Appraisal fees

- Home inspection costs

- Lender’s title insurance

- Credit report fees

- Homeowner’s insurance premiums

- Property tax prorations

Typical Seller Costs:

- Real estate agent commissions (usually 5-6% of sale price)

- Owner’s title insurance

- Transfer taxes

- Attorney fees

- Outstanding mortgage payoff

- Recording fees

The main difference isn’t who pays what, but how much it all adds up to. Home prices in Huntsville are usually higher than in Decatur, so percentage-based fees like commissions are larger there.

Both sides can negotiate who pays the closing costs, no matter the county. In a hot market, sellers might cover more costs to get the deal done. If things are slow, buyers may take on extra expenses.

Buyers in both counties generally pay 2-5% of the loan amount for closing costs. Sellers usually pay 6-10% of the sale price when you add up all the fees and commissions.

The actual numbers depend on property value, loan type, and whatever you work out in negotiations. Local customs don’t really change much between Madison and Morgan counties.

Estimated Closing Costs On A $300K Home (Huntsville Vs. Decatur)

If you’re buying a $300,000 home in Huntsville or Decatur, you’ll probably pay between $6,000 and $15,000 in closing costs. These fees usually range from 2% to 5% of the loan amount.

Huntsville Closing Cost Breakdown:

| Cost Item | Estimated Amount |

| Loan origination fee (1%) | $3,000 |

| Appraisal fee | $400-$600 |

| Title insurance | $1,200-$1,500 |

| Home inspection | $350-$500 |

| Recording fees | $100-$200 |

| Property taxes (prorated) | $500-$1,000 |

| Total Estimated | $8,550-$9,800 |

Decatur Closing Cost Breakdown:

| Cost Item | Estimated Amount |

| Loan origination fee (1%) | $3,000 |

| Appraisal fee | $400-$600 |

| Title insurance | $1,100-$1,400 |

| Home inspection | $300-$450 |

| Recording fees | $100-$200 |

| Property taxes (prorated) | $450-$900 |

| Total Estimated | $8,350-$9,550 |

Decatur’s closing costs usually run a bit lower than Huntsville’s. That’s mostly because property tax rates and inspection fees are a touch lower.

Don’t forget to budget for prepaid items like homeowners’ insurance and mortgage interest that add up between closing and your first payment. The loan origination fee is the fee the lender charges to process your loan.

Property taxes get divided up based on when you close. If you can negotiate seller concessions, you might reduce your out-of-pocket expenses at closing.

If rising costs or confusing fee sheets are overwhelming you, you’re not alone. Get honest answers and clear numbers with J. Wesley Atkinson guiding your next step. Schedule an appointment.

If you’re ready to get started, call us now!

Can You Reduce Closing Costs? (City Programs, Seller Credits, Lender Options)

There are actually a few ways buyers in Huntsville and Decatur can lower their closing costs. Sometimes these options save you thousands at the table.

Seller Credits

Ever heard of a seller credit? It’s a negotiation tactic where the seller agrees to pay part of your closing costs—often 2-3% of the home’s price.

This move works best if you’re in a buyer’s market and sellers need a nudge to get the deal done.

Lender Credits

You can also ask the lender for a loan. The lender covers some of your closing costs, but you take on a slightly higher interest rate.

It’s a tradeoff: less money upfront, but you’ll pay more over the life of the loan. This helps if you’re really focused on reducing those immediate expenses. Here’s more on how to reduce immediate closing expenses.

Local Assistance Programs

Alabama has down payment and closing cost assistance through the Alabama Housing Finance Authority.

Madison County and the City of Huntsville sometimes offer programs for first-time buyers or families with lower incomes.

Other Money-Saving Strategies

- Shop around: Comparing lenders can knock off hundreds in fees

- Close near month-end: You’ll owe less in prepaid interest

- Negotiate fees: Some lenders will lower or even drop application or processing charges if you ask

- Ask about no-closing-cost mortgages: These roll costs into your loan amount instead

Always request loan estimates from a few lenders, ideally all within a week or so. Comparing those documents will help you spot the best deal on both fees and rates.

Common Closing Cost Mistakes Buyers & Sellers Make In 2025

Lots of buyers forget to budget for the full amount of closing costs. They get so focused on the down payment that they overlook all the extra fees, which can lead to a cash crunch right before closing.

Not shopping around for services is another expensive error. You can usually pick your own title company, home inspector, and insurance provider. If you compare prices, you’ll likely save hundreds.

Sellers sometimes ignore closing costs because of state-to-state differences. Transfer taxes and government fees can vary a lot depending on where you’re selling. What’s true in one part of Alabama might not match up in another.

Here are some of the most common mistakes both buyers and sellers make:

- Waiting until the last minute to review the Closing Disclosure

- Not asking about unclear or duplicate fees

- Assuming every cost is fixed and can’t be negotiated

- Forgetting to ask the lender about no-closing-cost loan options

- Missing out on tax deductions for certain closing expenses

Buyers often just accept the first loan estimate they get, without comparing offers from other lenders.

Even small differences in interest rates and fees can add up over time. If you get at least three quotes, you’ll have a much better shot at finding the best terms.

Sellers sometimes agree to pay buyer concessions without realizing how much it’ll cut into what they actually take home. Those concessions come right off the top at closing.

Both buyers and sellers really need to understand what closing costs include well before closing day.

That way, there’s time to fix issues or negotiate better terms—nobody likes last-minute surprises.

Closing Cost Timeline: What Happens From Contract To Closing Day?

The closing process usually takes 30 to 60 days after both sides settle on terms. Most folks wrap up closing in about 45 to 50 days.

The timeline splits into a few big steps:

Weeks 1-2: Initial Steps

- Home inspection happens.

- Someone orders and completes the appraisal.

- The title search kicks off.

- Buyers start applying for homeowners’ insurance.

Weeks 3-4: Processing

- The lender reviews all your paperwork.

- Underwriting gets underway.

- The title company puts together closing documents.

- Any issues from inspection or appraisal get sorted out.

Week 5-6: Final Preparations

- Buyers do their final walkthrough.

- The closing disclosure is available at least three business days before closing.

- Buyers take a good look at all fees and loan terms.

- Wire transfers get set up for closing costs.

The closing disclosure is a big deal—buyers get it three days before closing. It spells out the loan terms, monthly payments, and closing costs. Buyers should really check it against their first loan estimate and watch for any surprises.

Most delays happen because someone forgot a document, made a last-minute change to their credit, or found something odd on the settlement statement.

Buyers can dodge headaches by answering lender questions fast and keeping their finances steady.

Ownership changes hands on closing day once everyone signs and the money moves. Buyers finally get the keys, and that’s when it feels real.

J. Wesley Atkinson understands how stressful hidden closing fees can feel. Don’t wait for last-minute surprises at the table—protect your budget and peace of mind. Contact us today.

Contact Us Today For An Appointment

Frequently Asked Questions

How much are closing costs in Huntsville and Decatur?

Expect buyers to pay about 2%–5% of the purchase price and sellers to pay about 6%–10%, depending on price, loan type, and negotiated credits — use a local calculator to get an exact number for your transaction.

Who usually pays the closing costs — the buyer or the seller?

Buyers normally pay loan-related fees (origination, appraisal), title/escrow lender charges, and prepaids; sellers usually pay agent commissions and owner’s title charges, plus prorated taxes and any negotiated concessions.

What specific fees should Huntsville/Decatur buyers budget for?

Budget for appraisal, lender origination/underwriting fees, lender title policy, escrow/closing fees, recording fees, and prepaid property taxes/insurance — these typically add up to the 2%–5% range.

What specific fees do sellers in Huntsville/Decatur usually pay?

Sellers most often pay real-estate commissions (the largest item), owner’s title policy/closing fees, prorated property taxes, and any transfer/recording fees or seller concessions agreed in the contract.

Can I reduce my closing costs in Decatur or Huntsville — and how?

Yes — options include seller credits negotiated in contract, lender credits, shopping multiple title/escrow providers, and local assistance programs (e.g., Decatur’s HOME/assistance options) for eligible buyers.

Are there county-specific fees or timeline traps I should know about?

Yes — Madison (Huntsville) and Morgan (Decatur) have specific recording and transfer fee schedules and different processing times, so request local fee schedules early and factor in recording turnaround to avoid last-minute delays.

What’s the fastest way to get an accurate closing cost estimate for my deal?

Ask your lender for a Loan Estimate and your title/escrow company for a local quote, or use a county-aware closing cost calculator (enter purchase price, loan details, and county) to produce buyer/seller line-by-line estimates you can verify with the settlement agent.