Get Legal Advice

(256) 993-5260

Alabama LLC vs S-Corp:

Originally published: May 2026 | Reviewed by J. Wesley Atkinson

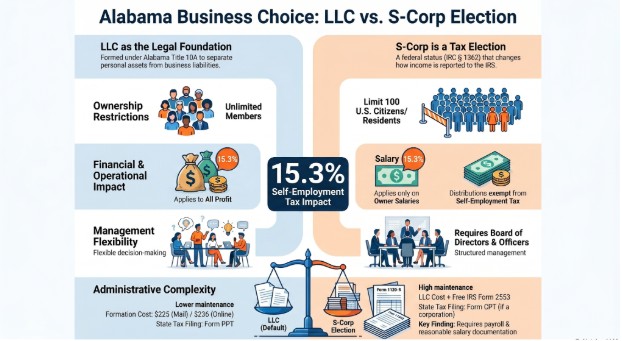

An Alabama LLC and an S-Corp are not competing entity types — an S-Corp is a federal tax election, not a separate legal structure. Alabama business owners choose between forming an LLC or a corporation under Title 10A of the Code of Alabama 1975, then decide separately how that entity is taxed at the federal level.

The right structure depends on the business’s net profit level, payroll obligations, ownership goals, and administrative capacity.

Atkinson Law’s business formation attorney evaluates both structures against a client’s specific income and ownership profile before recommending a formation path.

Key Takeaways

- An S-Corp is a federal tax classification elected through IRS Form 2553 under Internal Revenue Code § 1362, not a separate business entity under Alabama law

- An Alabama LLC taxed as a sole proprietorship or partnership pays self-employment tax on 100% of net profit; an LLC or corporation electing S-Corp status pays self-employment tax only on the owner-employee’s reasonable salary.

- Alabama LLCs file an Annual Business Privilege Tax Return (Form PPT) with ALDOR; Alabama corporations file Form CPT — both are governed by Alabama Code §§ 40-14A-21 through 40-14A-29

- Most CPAs recommend the S-Corp election when net annual profit consistently exceeds $40,000–$50,000 — the point at which payroll tax savings typically offset administrative overhead.

What Is the Difference Between an LLC and an S-Corp in Alabama?

An Alabama LLC is a legal entity formed under Title 10A of the Code of Alabama 1975 that separates the owner’s personal assets from business liabilities.

An S-Corp is a federal income tax election — governed by Internal Revenue Code § 1362 — that changes how the entity’s income is reported and taxed at the federal level.

A single business can be both an Alabama LLC and an S-Corp with the IRS.

| Feature | Alabama LLC (Default) | S-Corp Election |

| Legal structure | Formed under Title 10A, Code of Alabama 1975 | Federal tax status applies to an LLC or a corporation |

| Taxation | Pass-through; all net profit is subject to self-employment tax | Pass-through; only the owner’s salary is subject to payroll tax |

| Self-employment tax | 15.3% on 100% of net profit | 15.3% on salary only — distributions exempt |

| Formation cost | $236 online / $225 by mail | LLC formation cost + IRS Form 2553 (free) |

| Alabama Business Privilege Tax | Form PPT filed with ALDOR | Form CPT if structured as a corporation |

| Annual complexity | Low — minimal ongoing filings | High — payroll, reasonable salary documentation, Form 1120-S |

| Ownership restrictions | Unlimited members; no citizenship requirement | Maximum 100 shareholders; U.S. citizens/residents only |

| Management flexibility | Member-managed or manager-managed | Requires a board of directors and an officer structure |

How Are Alabama LLCs and S-Corps Taxed Differently?

An Alabama LLC taxed under default IRS rules passes all net profit directly to the member’s personal tax return — and the entire net profit is subject to the 15.3% federal self-employment tax, which covers Social Security and Medicare under the Self-Employment Contributions Act.

An LLC or corporation electing S-Corp status splits owner compensation into two components: a W-2 salary and profit distributions. Only the W-2 salary is subject to payroll taxes — distributions pass through to the owner tax-free of self-employment tax.

S-Corp payroll tax savings are real but depend entirely on net profit level and the defensibility of the owner’s reasonable salary documentation.

The IRS requires S-Corp owner-employees to pay themselves a reasonable compensation — a salary comparable to market rate for the same work — before taking distributions. Underpaying a salary to maximize distributions is an audit trigger.

Alabama business owners weighing this decision should review their structure with a North Alabama business attorney before filing the S-Corp election with the IRS.

If you’re ready to get started, call us now!

What Does an Alabama LLC vs. an S-Corp Cost to Maintain?

Formation cost is only the starting point. The ongoing administrative cost of an S-Corp election typically runs $1,000–$2,000 more per year than maintaining a standard Alabama LLC.

An LLC taxed as a sole proprietorship or partnership files Schedule C or Form 1065 annually — both are straightforward returns.

An S-Corp requires Form 1120-S, quarterly payroll tax deposits, W-2 issuance, and payroll tax filings — obligations that typically require a CPA or payroll service.

| Annual Cost Item | Alabama LLC (Default) | S-Corp Election |

| Alabama Business Privilege Tax | $50 minimum (Form PPT) per taxable year beginning after December 31, 2022, under Act 2022-252 | $50 minimum (Form PPT or CPT) per taxable year beginning after December 31, 2022, under Act 2022-252 |

| Federal tax return | Schedule C or Form 1065 | Form 1120-S |

| Payroll processing | Not required | Required — quarterly deposits + W-2 |

| CPA fees (estimated) | $500–$1,500/year | $1,500–$3,500/year |

| Registered agent | $0–$125/year | $0–$125/year |

| Total estimated annual overhead | $550–$1,625 | $1,550–$3,625 |

The cost gap between the two structures narrows as net profit grows. At $40,000–$50,000 net profit, the S-Corp’s payroll tax savings rarely offset the additional administrative cost.

At $80,000 net profit, the savings typically exceed overhead by a meaningful margin. Owners reviewing how to form an LLC in Alabama should factor ongoing maintenance costs into the formation decision before filing.

When Should an Alabama Business Choose an LLC?

An Alabama LLC with default tax treatment is the correct structure for most early-stage businesses, solo operators, real estate investors, and professional service providers whose net profit has not yet reached a level where S-Corp payroll tax savings offset administrative costs.

The LLC structure under Title 10A of the Code of Alabama 1975 provides full personal liability protection with the lowest formation cost, the fewest annual compliance obligations, and the most flexible ownership and management structure available under Alabama law.

Choose an Alabama LLC when:

- Net annual profit is consistently below $40,000–$50,000

- The business has one owner or a small number of members with no outside investors

- The owner wants member-managed flexibility without board or officer requirements

- The business involves real estate — Alabama LLCs provide stronger personal liability separation for property holdings than a sole proprietorship or general partnership.

- The owner is in the early stage of building revenue and wants minimal overhead.

- The business involves foreign nationals or non-resident owners — S-Corp eligibility is restricted to U.S. citizens and permanent residents.

Owners in this category should start by reviewing the full Alabama LLC formation process before engaging a formation attorney.

If you’re ready to get started, call us now!

When Should an Alabama Business Elect S-Corp Status?

An Alabama business should consider electing S-Corp status when net profit is consistent, the owner is actively working in the business, and the projected payroll tax savings on distributions exceed the additional cost of payroll processing and a more complex annual tax return.

The IRS requires the S-Corp election to be filed on Form 2553 no later than two months and fifteen days after the beginning of the tax year in which the election is to take effect — a deadline that Alabama business owners frequently miss.

Choose S-Corp election when:

- Net annual profit consistently exceeds $40,000–$50,000

- The owner draws a salary from the business and can document reasonable compensation

- The business has no more than 100 shareholders, all of whom are U.S. citizens or permanent residents

- The owner has engaged a CPA familiar with Alabama and federal S-Corp compliance requirements

- The business is structured as an LLC, and the owner wants to retain LLC flexibility while capturing S-Corp tax savings

Electing S-Corp status at the right profit threshold reduces the owner’s annual federal self-employment tax liability, allowing the business to retain more net income without restructuring operations.

Atkinson Law’s formation counsel includes a structure review to determine whether an S-Corp election is appropriate at formation or should be deferred until the business reaches a qualifying profit threshold.

Common Mistakes When Choosing Between LLC and S-Corp in Alabama

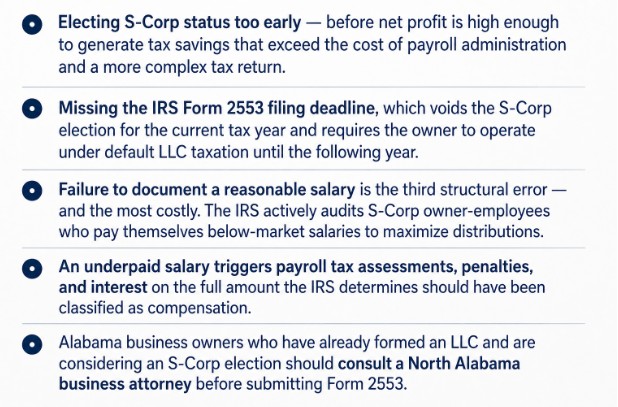

Alabama business owners make three common structural errors when choosing between an LLC and an S-Corp. The first is electing S-Corp status too early — before net profit is high enough to generate tax savings that exceed the cost of payroll administration and a more complex tax return.

The second is missing the IRS Form 2553 filing deadline, which voids the S-Corp election for the current tax year and requires the owner to operate under default LLC taxation until the following year.

Failure to document a reasonable salary is the third structural error — and the most costly. The IRS actively audits S-Corp owner-employees who pay themselves below-market salaries to maximize distributions.

An underpaid salary triggers payroll tax assessments, penalties, and interest on the full amount the IRS determines should have been classified as compensation.

Alabama business owners who have already formed an LLC and are considering an S-Corp election should consult a North Alabama business attorney before submitting Form 2553.

Contact Us Today For An Appointment

Frequently Asked Questions

Can an Alabama LLC elect S-Corp tax treatment?

An Alabama LLC may elect S-Corp federal tax treatment by filing IRS Form 2553 with the Internal Revenue Service. The election must be filed no later than two months and fifteen days after the start of the tax year in which the election takes effect. The LLC retains its legal structure under Title 10A — only its federal tax classification changes.

What is the S-Corp’s reasonable salary requirement in Alabama?

The IRS requires every S-Corp owner-employee to receive a W-2 salary comparable to the market rate for the same services under Internal Revenue Code § 1366 and IRS reasonable compensation guidance. Alabama S-Corp owners who pay themselves below-market salaries are subject to payroll tax assessments, penalties, and interest on the reclassified compensation amount.

Does Alabama recognize S-Corp status for state tax purposes?

Alabama follows the federal S-Corp election for state income tax purposes — S-Corp income passes through to individual shareholders’ Alabama income tax returns. Alabama S-Corps file Form 20S with the Alabama Department of Revenue annually. The Alabama Business Privilege Tax applies to both LLCs and S-Corps under Alabama Code §§ 40-14A-21 through 40-14A-29, regardless of federal tax classification.

When is the deadline to elect S-Corp status for an Alabama LLC?

The IRS requires Form 2553 to be filed no later than two months and fifteen days after the first day of the tax year in which the election is to take effect. For a calendar-year LLC, the deadline is March 15. An election filed after that date takes effect the following tax year unless the IRS grants late election relief under Revenue Procedure 2013-30.

How does Alabama’s Business Privilege Tax apply to S-Corps vs LLCs?

Both Alabama LLCs and S-Corps are subject to the Alabama Business Privilege Tax filed annually with ALDOR under Alabama Code §§ 40-14A-21 through 40-14A-29. LLCs file Form PPT, and S-Corps are structured as corporations that file Form CPT. The minimum tax is $50 per taxable year beginning after December 31, 2022, under Act 2022-252. Entities whose calculated tax is $100 or less are fully exempt from filing and payment.

What is the difference between an LLC and a corporation in Alabama?

An Alabama LLC is formed under Title 10A of the Code of Alabama 1975 and offers flexible member-managed or manager-managed governance with no board requirement. An Alabama corporation requires a board of directors, officer appointments, and documentation of annual meetings. Both entity types provide personal liability protection but differ in management structure and ongoing compliance obligations.

Can an Alabama S-Corp have more than one owner?

An Alabama S-Corp may have up to 100 shareholders under Internal Revenue Code § 1361. All shareholders must be U.S. citizens or permanent residents — non-resident aliens are ineligible. Husband-and-wife shareholders count as one shareholder for the 100-shareholder limit. An LLC electing S-Corp status must satisfy these ownership restrictions to maintain the election.

What Alabama state tax forms does an S-Corp file?

An Alabama S-Corp files Form 20S with the Alabama Department of Revenue for state income tax purposes annually. The S-Corp also files Form PPT or Form CPT for the Alabama Business Privilege Tax with ALDOR under Alabama Code §§ 40-14A-21 through 40-14A-29. Both returns are due by the same date as the corresponding federal income tax return.

J. Wesley Atkinson, Attorney at Law, represents individuals and businesses in North Alabama real estate closings, business formation, and estate planning matters across Huntsville, Decatur, and Madison County. To discuss LLC vs S-Corp structure with Atkinson Law, contact the Huntsville office.