Get Legal Advice

(256) 993-5260

Originally published: April 2025 | Reviewed by J. Wesley Atkinson

Closing day is when you finally become a homeowner! It’s the day when all the paperwork gets signed, money changes hands, and you receive the keys to your new property.

The closing process typically involves meeting with professionals such as your real estate agent, a representative from the title company, and possibly attorneys, depending on your location.

Before this important day arrives, you’ll need to review your closing disclosure, arrange for payment of closing costs, and complete a final walkthrough of the property to ensure everything is as agreed.

At the closing meeting, you’ll sign legal documents transferring ownership, pay closing costs and escrow items, and complete the final steps in your home-buying journey.

Key Takeaways

- Closing day transfers property ownership through document signing and payment of closing costs.

- Participants typically include buyers, sellers, real estate agents, lenders, and title company representatives.

- Preparing properly with document reviews and final walkthroughs helps prevent delays and ensures a smooth transaction.

Real Estate Closings In Decatur, AL – What Buyers And Sellers Should Know

A real estate closing marks the final stage of a property transaction—the moment when legal ownership officially passes from the seller to the buyer.

In Decatur, closings typically occur at a title company or an attorney’s office. During this meeting, all parties sign the necessary legal documents, and the buyer provides payment.

The closing process in Decatur involves several key participants:

- Buyers and sellers

- Real estate agents

- Closing attorney

- Lender representative (if financing is involved)

- Title company representative

Buyers should come prepared with a valid photo ID and certified funds for the closing costs.

The final walk-through usually happens 24 hours before closing to verify that the property’s condition matches the agreement terms.

Why Closings Differ By State (And What That Means In Alabama)

Alabama follows different closing practices than many other states, which affects how transactions conclude in Decatur.

Alabama is a “title theory” state, meaning the lender holds the property title until the mortgage is paid off.

In Decatur, real estate closings require an attorney’s involvement, unlike some states where only escrow agents are needed.

This provides additional legal protection for both parties. Alabama law also has specific requirements about disclosure documents that sellers must provide.

The closing process in Alabama typically takes 30-45 days from the accepted offer to the closing day.

Decatur buyers should know that Alabama is an “attorney state,” requiring legal professionals to handle title examinations and prepare closing documents.

Who’s Involved At A Decatur Real Estate Closing

A real estate closing in Decatur brings together several key participants who each play vital roles in finalizing the property transfer.

The exact mix of people at your closing table depends on your specific transaction, but certain individuals are almost always present.

Buyer And Seller

Buyers and sellers are the primary parties in any Decatur real estate transaction. Buyers must bring a photo ID and certified funds for their closing costs.

They’ll sign numerous documents, including the mortgage agreement, promissory note, and deed transfer papers.

Sellers must provide identification and bring all house keys, garage door openers, and access codes.

They’ll sign the deed transferring ownership and other closing documents. Sometimes, sellers pre-sign papers and don’t physically attend the closing.

In Decatur, both parties should review the closing disclosure at least three days before the meeting. This gives everyone time to address discrepancies or ask questions about unexpected costs.

Most buyers and sellers in Decatur choose to attend the closing in person, but proxy closings are possible with proper power-of-attorney documentation.

Real Estate Agent(s)

Buyers and sellers’ real estate agents typically attend the Decatur closing to protect their clients’ interests. These professionals help explain complex documents and terms during the closing process.

Agents verify that all negotiated repairs and contingencies have been addressed before closing. They also confirm that the final paperwork correctly reflects any credits or prorations.

In Decatur closings, agents often:

- Review final documents for accuracy

- Address last-minute questions

- Provide the necessary paperwork from the transaction

- Hand over keys once the closing is complete

The listing agent ensures the seller understands what they’re signing and that all seller obligations have been met. The buyer’s agent confirms that their client receives everything the purchase agreement promises.

Real estate agents typically receive their commissions through closing, with funds disbursed by the closing agent or attorney.

Closing Attorney Or Title Company Representative

In Decatur, Georgia, closings are typically handled by an attorney rather than an escrow company.

This closing attorney acts as a neutral third party who prepares documents and oversees the legal transfer of property.

The closing attorney or title company representative:

- Performs title searches to ensure clear ownership

- Prepares closing documents and explains them to all parties

- Collects and distributes funds according to the settlement statement

- Record new deed and mortgage documents with county officials

- Issues with title insurance protecting the buyer and lender

They coordinate with all parties to schedule the closing appointment and ensure all required documents are ready.

The closing attorney verifies that taxes are current and handles any tax prorations between the buyer and seller.

In Decatur, the closing attorney manages the escrow account where earnest money is held. They ensure all funds are properly disbursed according to the closing process requirements.

Mortgage Lender Or Broker

A mortgage lender representative may attend the Decatur closing, particularly for more complex transactions.

Their role is to ensure that all loan documents are properly executed and that all lending conditions are satisfied.

The lender or broker confirms that:

- All loan documents are signed correctly

- Insurance requirements are met

- Property appraisal meets lending standards

- Down payment funds are properly sourced

- Closing costs match the loan estimate

Mortgage brokers sometimes attend to help explain loan terms and payment schedules. They can clarify questions about interest rates, escrow accounts, and future mortgage responsibilities.

In some Decatur closings, the lender participates remotely, sending documents to the closing attorney beforehand. The closing attorney then acts as the lender’s agent during document signing.

First-time homebuyers especially benefit from having their mortgage representative present to explain complex financing terms.

Sometimes Present: Surveyors, Home Inspectors

While not typically at the closing table, surveyors and home inspectors play important roles leading to Decatur closings. Their work is often referenced during the final transaction.

Surveyors determine exact property boundaries and identify any encroachments or easements. Their reports become part of the closing documentation and may be discussed if boundary issues exist.

Home inspectors rarely attend closings, but their reports influence negotiations that impact closing terms. The final settlement will reflect any repair agreements based on inspection findings.

Other professionals who might occasionally attend Decatur closings include:

- Interpreters for non-English speaking participants

- Contractors to verify completed repairs

- Tax professionals for complex tax implications

- Family members or advisors supporting buyers/sellers

In special circumstances, property specialists like termite inspectors may need to provide final clearance documentation at closing.

These situations are more common in Decatur’s historic neighborhoods, where older homes may have specific inspection requirements.

The Pre-Closing Checklist – What To Do Before The Big Day

Preparing for your real estate closing requires careful attention to several critical tasks. Taking care of these items before the big day will help ensure a smooth, stress-free closing experience.

Review The Closing Disclosure (CD)

Your lender will provide a Closing Disclosure at least three business days before closing. This important document outlines the final terms of your mortgage loan, including:

- The loan amount and interest rate

- Monthly payment breakdown

- Closing costs and fees

- Cash needed to close

Compare this document carefully with your Loan Estimate to spot any unexpected changes or errors. If you find discrepancies, contact your lender immediately to resolve them.

The three-day window isn’t just a courtesy—it’s required by law to give you time to understand the terms before you’re legally bound to them.

Use this time wisely to ask questions about anything that seems unclear or different from what you expected.

Confirm Payment Method For Closing Costs

Closing costs typically range from 2-5% of the loan amount, and you’ll need to arrange payment before the closing day arrives. Personal checks are rarely accepted for these transactions.

Most title companies and attorneys require payment via:

- Cashier’s check from your bank

- Wire transfer directly to the closing agent

If you plan to use a wire transfer, contact your bank a few days in advance to understand their process. Wire transfers can take 24-48 hours, so timing is crucial.

Be extremely cautious about wire instructions received via email. Wire fraud is common in real estate transactions. Always verify the receiving account information by phone using a number you’ve independently confirmed.

Final Walkthrough Of The Property

Schedule a final walk-through within 24 hours of closing.

This isn’t a second home inspection, but rather a verification that:

- The property’s condition hasn’t changed since your inspection

- Agreed-upon repairs have been completed

- The sellers have fully vacated (unless otherwise arranged)

- All included appliances and fixtures remain in the home

Bring your purchase agreement and inspection reports to ensure all conditions are met.

Test all appliances, light switches, and plumbing fixtures.

If you discover problems during the walkthrough, discuss them with your real estate agent immediately.

Minor issues can be resolved with an adjustment at closing, while major problems might require delaying the closing until they’re addressed.

Are you starting a new venture in Huntsville? Before buying property, consult with J. Wesley Atkinson Law Firm about incorporating your business the right way—secure, structured, and legally sound.

If you’re ready to get started, call us now!

What To Expect On Closing Day

Closing day marks the final step in your home-buying journey when you officially become the homeowner.

The process typically takes a few hours and involves several important steps to transfer ownership properly.

Where It Happens

Closings usually take place at a neutral location such as a title company office, escrow company, or attorney’s office.

Some lenders may allow you to close at their location. In recent years, remote notarization options have become more widely available, allowing buyers to sign documents electronically.

Your real estate agent or lender will inform you of the closing location. It’s best to arrive 15 minutes early to allow time for any unexpected delays.

If you can’t attend in person, you can authorize someone else to sign on your behalf using a power of attorney.

This option requires planning and approval from your lender.

What To Bring With You

Being prepared for closing day helps ensure a smooth process. Here’s what buyers should bring:

- Government-issued photo ID (driver’s license, passport)

- Cashier’s check or wire transfer confirmation for closing costs

- Proof of homeowners insurance

- Final closing disclosure (sent at least 3 days before closing)

- Questions you want answered before signing

The exact amount needed for closing will be provided in your closing disclosure.

Funds typically need to be in the form of a certified check or wire transfer – personal checks are rarely accepted for large amounts.

Don’t forget to bring your checkbook for any small last-minute adjustments to closing costs. These unexpected costs are rare but can happen.

Signing The Documents

The loan closing involves signing numerous legal documents. A typical closing package contains 50-100 pages of documents that transfer ownership and finalize your mortgage. Key documents include:

- Closing Disclosure – Details final loan terms and closing costs

- Promissory Note – Your promise to repay the loan

- Deed of Trust/Mortgage – Secures the loan using the home as collateral

- Deed – Transfers ownership from seller to buyer

A notary public will verify your identity and witness your signatures.

Don’t hesitate to ask questions if anything is unclear. You have the right to review all documents before signing.

Review important details about your interest rate, loan amount, and payment schedule. The closing agent will guide you through each document.

Disbursing The Funds

Once the documents are signed, funds are distributed to the appropriate parties.

During this part of the closing process, several financial transactions occur:

- The buyer’s down payment and closing costs are collected

- The lender releases the mortgage loan funds

- The seller receives their proceeds from the sale

- Various third parties receive their fees (title company, attorneys, real estate agents)

The funds typically move through an escrow account managed by the closing agent. This ensures all parties are paid correctly and simultaneously.

If there are any issues with the fund transfers, the closing may be delayed until they’re resolved.

Most closings conclude successfully on the scheduled closing date.

Recording The Deed

The final step in the closing process is recording the deed with the local government.

After signing, the closing agent will:

- Submit the deed to the county recorder’s office

- Pay any required recording fees

- Establish a public record of the ownership transfer

This recording process typically happens within a few days after closing.

Some title companies will handle this immediately after the closing meeting, while others process it the next business day.

Once recorded, the deed becomes a public record, officially documenting you as the new owner. The original deed will be mailed to you several weeks after closing.

In some areas, you might receive the keys immediately after signing, while in others, the seller might retain possession briefly based on your purchase agreement.

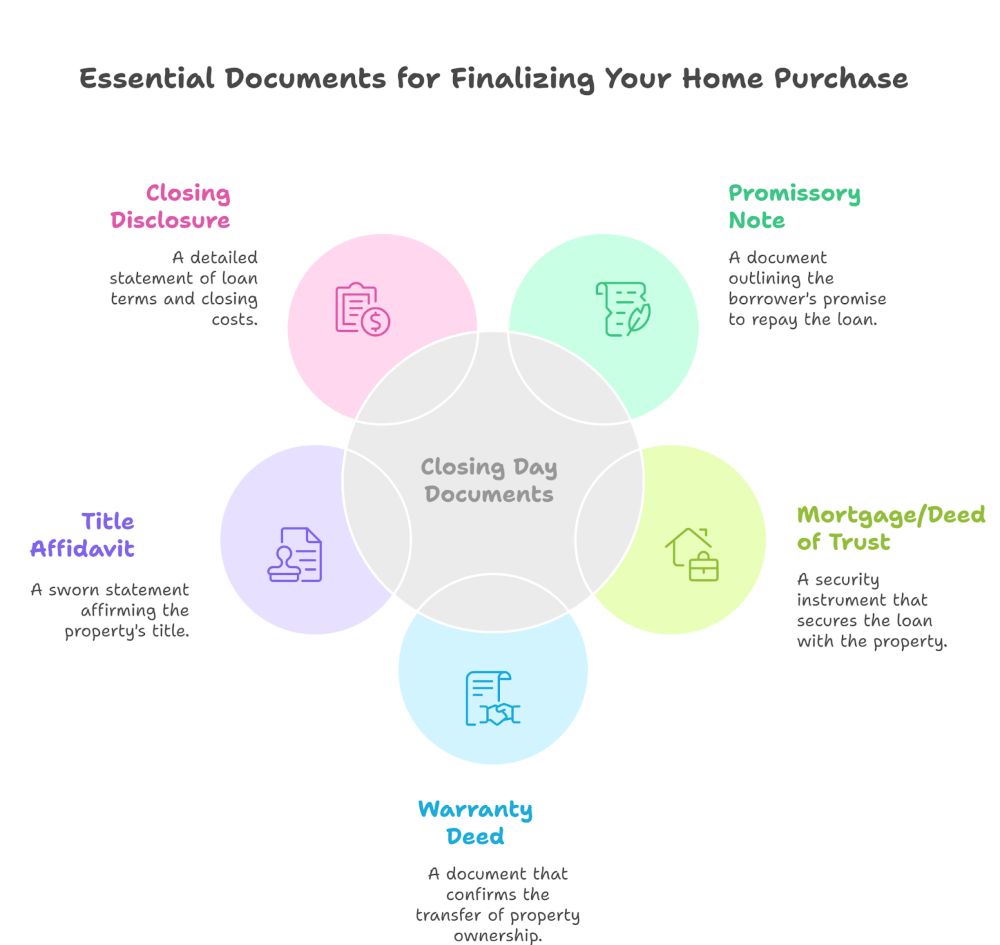

Key Documents You’ll Review And Sign

On closing day, you will sign several critical legal documents that finalize your home purchase and establish your responsibilities as a homeowner.

These papers transfer ownership and outline the terms of your mortgage agreement.

Promissory Note

The promissory note is a legal document that details your promise to repay your mortgage loan. This document specifies:

- Loan amount: The total sum you’re borrowing

- Interest rate: Fixed or adjustable rate percentage

- Repayment period: Typically 15 or 30 years

- Payment schedule: Monthly due dates

- Penalties: Fees for late or missed payments

The promissory note indicates your debt and the lender’s right to collect payment. It also outlines what happens if you default on the loan.

Buyers should carefully review the interest rate and payment terms to ensure they match what was initially agreed upon with the lender.

Mortgage Or Deed Of Trust (Security Instrument)

The mortgage or deed of trust is the security instrument that puts your property up as collateral for your loan.

This document gives the lender the right to foreclose on your home if you fail to make payments as specified in the promissory note.

Key elements include:

- Property description

- Borrower and lender information

- Rights and responsibilities of both parties

- Default provisions

- Acceleration clause (making the entire loan due immediately upon default)

The main difference between a mortgage and a deed of trust is how foreclosure works.

A mortgage requires judicial foreclosure through the court, while a deed of trust allows for a faster, non-judicial foreclosure process.

This document will be recorded with the county clerk or recorder after closing.

Warranty Deed

The warranty deed is the legal instrument that transfers property ownership from the seller to you.

This crucial document provides several guarantees from the seller, including:

- Clear title to the property (free from undisclosed liens)

- Protection against claims from third parties

- Confirmation that the seller has the legal right to sell the property

The deed includes:

- Legal property description

- Names of both the seller (grantor) and the buyer (grantee)

- Date of transfer

- Signature of the seller

After signing, the county recorder’s office will record the warranty deed, making your ownership a public record. This recording establishes your legal rights to the property and protects against future ownership disputes.

Title Affidavit

The title affidavit (sometimes called a seller’s affidavit or owner’s affidavit) is a sworn statement from the seller confirming several important facts about the property:

- No outstanding judgments or liens exist against the property

- No boundary disputes or unrecorded easements are known

- No pending bankruptcy proceedings affect the property

- No knowledge of environmental contamination exists

- No construction work has been performed recently that could result in mechanics’ liens

This document protects both the title company and the buyer from undisclosed issues. It helps the title company issue clear title insurance by reducing the risk of unknown claims.

The title affidavit is signed under penalty of perjury, which means the seller can face legal consequences for providing false information.

Closing Disclosure And Settlement Statement (HUD-1 Alternative)

The Closing Disclosure is a five-page form that provides the final details about your mortgage loan and closing costs.

Lenders must provide this document at least three business days before closing, giving you time to review the terms carefully.

Key information includes:

- Loan terms: Interest rate, monthly payments, prepayment penalties

- Loan costs: Origination charges, services you can’t shop for, services you can shop for

- Other costs: Taxes, prepaids, initial escrow payments, other fees

- Cash to close: Total amount needed at closing

The Settlement Statement itemizes all charges and credits to the buyer and seller.

This document shows the amount you must bring to closing, usually through a certified check or wire transfer.

Compare this final disclosure to the Loan Estimate you received when you applied for your mortgage to identify any changes.

Are you thinking ahead to your next agreement? J. Wesley Atkinson Law Firm can assist with solid, reliable contract formation to protect your interests before, during, and after the closing table.

If you’re ready to get started, call us now!

How Much Will You Pay Or Receive At Closing?

Closing costs can range from 2% to 5% of the loan amount, and buyers and sellers are each responsible for different fees.

Understanding these costs will help you prepare financially and avoid surprises on closing day.

Common Closing Costs For Alabama Buyers

Alabama homebuyers typically pay several standard closing costs.

The loan origination fee usually ranges from 0.5% to 1% of your loan amount and compensates the lender for processing your mortgage.

Depending on your loan type, your down payment is the largest expense, typically 3% to 20% of the purchase price. This payment is separate from your earnest money deposit, which is applied toward your closing costs.

Other common fees include:

- Appraisal fee: $300-$500

- Credit report fee: $25-$50

- Title search and insurance: $700-$900

- Loan discount points: Optional fees to lower your interest rate (1 point = 1% of loan amount)

You’ll also fund your escrow account at closing, which covers property taxes and homeowners insurance for the first few months.

Seller Closing Costs And Net Sheet

Sellers receive a net sheet that outlines their proceeds after deducting closing costs. The largest deduction is typically the mortgage payoff amount.

Sellers in Alabama commonly pay:

- Real estate agent commissions (5-6% of sale price)

- Title insurance for the buyer (customary in some counties)

- Home warranty is negotiated in the contract

- Prorated property taxes and HOA dues

The purchase price minus these expenses equals the seller’s net proceeds.

Sellers should request their net sheet several days before closing to avoid surprises.

Most sellers receive their funds via wire transfer within 24 hours of closing. If the property sells for less than the mortgage owed, the seller must bring funds to closing.

Alabama Transfer Taxes

Alabama charges a deed recording tax when a property changes hands. This tax equals $0.50 per $500 of property value (or 0.1% of the purchase price).

For example:

| Home Price | Transfer Tax |

| $200,000 | $200 |

| $300,000 | $300 |

| $400,000 | $400 |

The seller typically pays this tax, but payment responsibility can be negotiated in the purchase agreement.

Some Alabama counties or municipalities add their own transfer taxes or recording fees on top of the state tax. For example, Jefferson County charges additional recording fees.

Transfer taxes must be paid before the deed can be recorded, officially transferring ownership to the buyer. The closing attorney or title company handles this payment from the closing proceeds.

Common Issues That Can Delay Closings

The closing day for a real estate transaction can be postponed by several unexpected hurdles that buyers and sellers should prepare for.

Understanding these potential roadblocks can help parties navigate the closing process more smoothly.

Title Defects Or Liens

Title issues are among the most common reasons for closing delays. These problems emerge during the title search when unexpected claims against the property are discovered.

Common title defects include:

- Outstanding tax liens

- Mechanic’s liens from unpaid contractors

- Judgment liens from court cases

- Undisclosed easements

- Errors in public records

Many sellers are unaware of existing liens on their property. When these issues surface, closing must be postponed until the seller can provide a clear title.

The title company typically requires all liens to be paid and released before closing can proceed. Depending on the issue’s complexity and how quickly the seller can address it, this process may take days or weeks.

Financing Problems Or Last-Minute Credit Checks

Mortgage issues frequently cause closing delays. Even buyers who received pre-approval might encounter problems at the final stages.

Common financing hurdles include:

- Changes in employment status between pre-approval and closing

- Recent large purchases that affect the debt-to-income ratio

- New credit inquiries or accounts opened during the mortgage process

- Failed mortgage underwriting

- Insufficient funds for down payment or closing costs

Lenders typically perform last-minute credit checks just before closing. Any negative changes can cause them to reconsider loan terms or withdraw approval entirely.

Buyers should avoid making major purchases, changing jobs, or applying for new credit between the loan application and closing.

They should also promptly submit all required documentation to the lender to prevent delays.

Appraisal Discrepancies

When a home’s appraisal comes in lower than the agreed purchase price, it creates significant complications.

Lenders will only finance a property up to its appraised value, creating a gap that must be addressed before closing.

This situation typically leads to one of several outcomes:

- Buyer brings additional cash to cover the difference

- Seller agrees to lower the price to match the appraisal

- Buyer and seller negotiate to split the difference

- The transaction falls through if no agreement can be reached

Other appraisal-related delays include the need for repairs identified during the home inspection or appraisal process.

If an appraiser notes safety issues or property damage, the lender may require fixing these before finalizing the loan.

Scheduling challenges with appraisers can also cause delays, especially during busy market periods when qualified appraisers are in high demand.

Wire Transfer Delays Or Mistakes

Financial transactions at closing can create last-minute complications. Buyers who fail to bring certified checks or proper payment forms may cause immediate delays.

Wire transfer issues include:

- Incorrect banking information

- Transfer cutoff times at financial institutions

- Processing delays between banks

- Cybersecurity verification procedures

To avoid these problems, buyers should verify wire instructions directly with the closing agent by phone.

They should also initiate transfers at least one business day before closing.

Different banks have different processing times for wire transfers. Some may complete transfers within hours, while others require a full business day or more, especially for large amounts, which is typical in real estate transactions.

Buyers should also be aware of daily transfer limits that might require special arrangements with their bank for the substantial sums involved in home purchases.

What Happens After The Closing?

After the real estate closing finishes, several important steps occur to complete the property transfer process. These steps formalize ownership and give the buyer full access to their new home.

Title Is Officially Recorded

Once the closing meeting ends, the title company or attorney will file the deed and mortgage documents with the local government recording office.

This official recording typically happens within a few business days after closing.

The recording process creates a public record showing the property’s new owner. Until this recording is complete, the buyer isn’t technically the legal owner yet, even though they’ve signed all the paperwork.

Some counties have electronic recording systems that process documents on the same day, while others may take several days to complete the recording.

Buyers can check with their title company or attorney about the expected timeline for their specific location.

Buyer Receives The Keys

The transfer of house keys typically happens on the possession date, usually the same day as the closing.

The seller hands over all house keys, garage door openers, mailbox keys, and security codes.

The keys might be transferred later if the seller negotiated to stay in the property after closing.

This arrangement, called a “rent-back agreement,” should be clearly outlined in the purchase contract.

Before moving in, buyers should:

- Change all locks for security

- Test all keys and garage door openers

- Update security codes or systems

- Notify the post office of their address change

Store Your Documents Safely

During closing, buyers receive numerous important documents related to their home purchase. These papers need proper storage for future reference.

Key documents to keep include:

- Closing Disclosure: Details all financial aspects of the transaction

- Promissory Note: The loan agreement with your lender

- Deed: Proves ownership of the property

- Title Insurance Policy: Protects against ownership claims

Consider scanning these documents and storing digital copies in a secure cloud service.

Keep original papers in a fireproof safe or safety deposit box.

These documents will be needed for tax purposes, future refinancing, or property sales.

Remember to store contact information for the title company, lender, and real estate agents along with these documents in case questions arise later.

Tips For A Smooth Closing In Decatur, AL

Proper preparation and local expertise can make all the difference when closing a property in Decatur.

These practical steps will help buyers and sellers navigate Alabama’s unique closing requirements while avoiding common delays.

Choose A Local Closing Attorney Familiar With Alabama Law

Selecting an attorney with specific experience in Decatur real estate transactions is crucial.

Alabama is an attorney-closing state, meaning lawyers handle the closing process rather than title companies in many cases.

A local attorney will understand Morgan County’s specific requirements and potential title issues that commonly arise in Decatur properties.

They can navigate local zoning regulations and ensure all documents comply with Alabama law.

Look for attorneys who regularly work with your preferred lender, which can streamline communication.

Many experienced closing attorneys in Decatur have established relationships with local banks and mortgage companies.

Ask your real estate agent for recommendations of attorneys who have successfully handled similar transactions in neighborhoods like Point Mallard, Albany, or Downtown Decatur.

Stay In Communication With Your Agent And Lender

Regular communication prevents last-minute surprises that could delay closing. Check your email daily and respond promptly to your lender’s and agent’s requests.

Lenders may need various documents, sometimes with tight deadlines.

Set calendar reminders for important dates like the appraisal, home inspection, and final walkthrough.

Create a dedicated folder (physical or digital) for all closing-related paperwork. This organization helps when you need to reference or provide information quickly.

Be especially vigilant about communication in the final week before closing. Many issues appear when lenders perform the last verification checks in these final days.

Consider setting up a group text or email thread with all key parties to ensure everyone stays informed of progress and potential issues.

Be Ready For Last-Minute Requests Or Changes

Flexibility is essential as closing approaches. Make sure all contingencies are addressed, and also, make sure you’ve received final mortgage approval before closing day.

Carefully review your closing disclosure when it arrives. The disclosure usually arrives three days before closing. Compare it to your loan estimate. Then, question any significant differences.

Prepare for potential closing costs specific to Decatur:

- Document stamps on deeds ($0.50 per $500 of property value)

- Recording fees

- Attorney fees (usually higher than in non-attorney states)

- Property tax prorations (Morgan County’s tax year)

Schedule time off work for the closing day and possibly the day after. Closing appointments typically last about 60 minutes, but delays can occur, especially for afternoon closings.

Ready to close with confidence? Let J. Wesley Atkinson Law Firm handle your real estate closing in Huntsville with precision, professionalism, and personal attention. Schedule your consultation today.

Contact Us Today For An Appointment

Frequently Asked Questions

How long does a real estate closing typically take in Decatur, AL

Most closings in Decatur take about 30 to 60 days from contract to close, depending on loan approval, title search, and property inspections. The actual closing appointment usually lasts 1 to 2 hours.

Do I need a real estate attorney to close on a home in Alabama?

Yes. Alabama is an “attorney state,” meaning a licensed Alabama attorney must be involved in the closing process—typically handling the paperwork, title examination, and funds disbursement.

Where do closings usually happen in Decatur?

Real estate closings in Decatur are typically held at the office of a closing attorney or title company, not at the home or real estate agent’s office.

Can I close on a home remotely in Alabama?

Remote closings are possible, but Alabama law may require in-person notarization for some key documents. Talk to your closing attorney to see if e-signature or remote notarization options are available for your transaction.

What should I bring to closing day in Decatur?

You’ll need a valid government-issued ID, certified funds or wire transfer confirmation, proof of homeowner’s insurance, and any documents your lender or attorney requests ahead of time.

What happens if something goes wrong at closing?

The closing may be postponed if issues like funding delays, title problems, or missing paperwork arise. Your closing attorney or agent will coordinate rescheduling and help resolve the issue quickly.

Who pays the closing costs in Alabama?

Typically, buyers cover loan-related fees and inspections, while sellers cover agent commissions and title transfer fees. However, closing costs are negotiable and vary by contract.